LeaseCrunch Blog

Read about ASC 842 & other lease accounting topics

You might know what GASB 87 is, but when it comes to making your lease accounting practices GASB 87 compliant, are you really hitting the ball out of the park? Read on for a GASB 87 implementation guide that includes a refresh on what GASB 87 requires of all US state and local governments (just in case you forgot), as well as tips for proper implementation of this new method of lease accounting.

GASB 87 is a part of the generally accepted accounting principles (GAAPs) outlined by the Governmental Accounting Standards Board (GASB). These rules must be followed by US state and local governments. Depending on the circumstances, it can also apply to certain non-profit organizations and municipal entities such as airports.

These principles and standards are not only recognized as authoritative by state and local governments but also by entities such as state boards of accountancy and the American Institute of Certified Public Accountants (AICPA).

The exemptions and exceptions to GASB 87 are:

GASB 87 is a statement issued by the GASB that requires the recognition of all an entity’s lease assets and liabilities that exceed 12 months in length. These assets and liabilities must now be recorded as lease liabilities and lease assets on financial statements.

Furthermore, GASB 87 expands the breadth of the leases that have to be accounted for in a way similar to how capital leases were previously documented. However, the title and concept of a “capital lease” has now been eliminated and replaced with the idea that all leases are recognized purely by the fact that they are financings of the right to use an asset.

GASB 87 is effective for fiscal years starting after June 15, 2021, with restatement required unless not practicable. Any entity with qualifying leases must document them underGASB 87 using the single model of lease accounting laid out in the GASB 87 declaration.

What follows are two GASB 87 lease examples, one for lessor accounting and the second for lessee accounting.

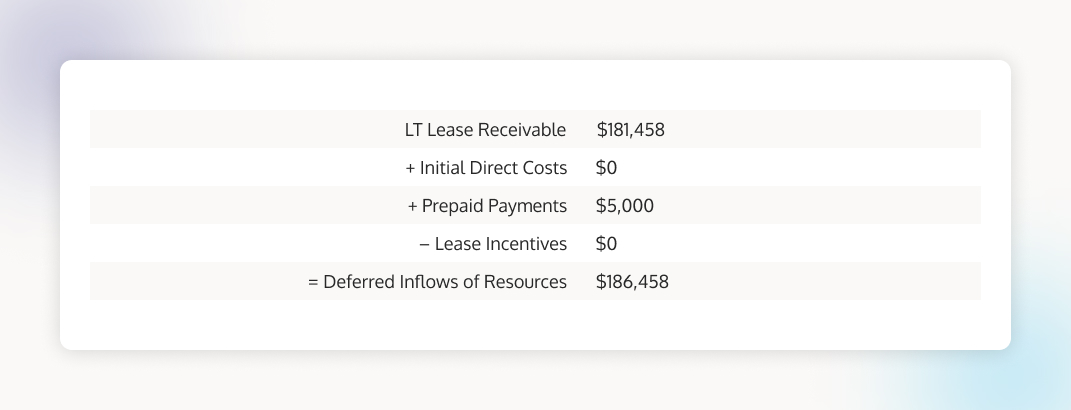

In this case, we have a lease that begins January 1st, 2024. Our discount rate is 4% and the term is 3 years. Monthly payments are going to be $5000 and increase $500 annually. The long term lease receivable will be recorded as the present value of future payments, and any prepayments or initial direct costs also must be accounted for, less any lease incentives. This results in the deferred inflows of resources.

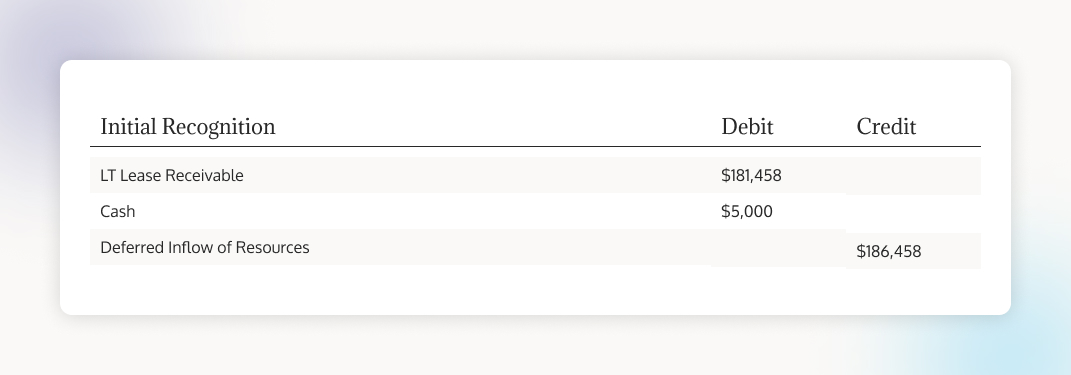

To record the journal entry, debit to the long term lease receivable and cash because that cash is received from the lessee. The deferred inflow of resources must be credited as well.

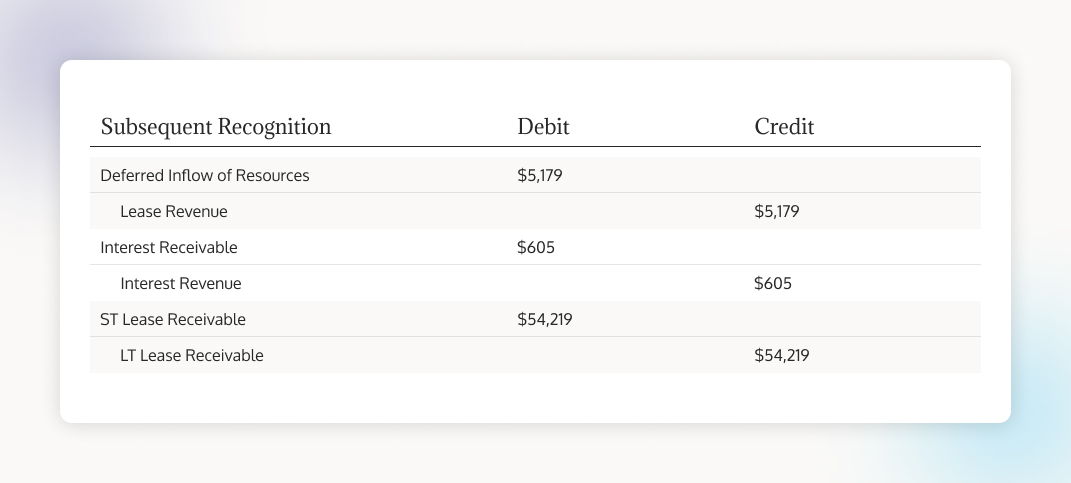

Below is the month one entry so the straight line revenue of our deferred inflow is $5179. Additionally, what one is expected to receive in the next 12 months as the short term lease receivable must also be recorded.

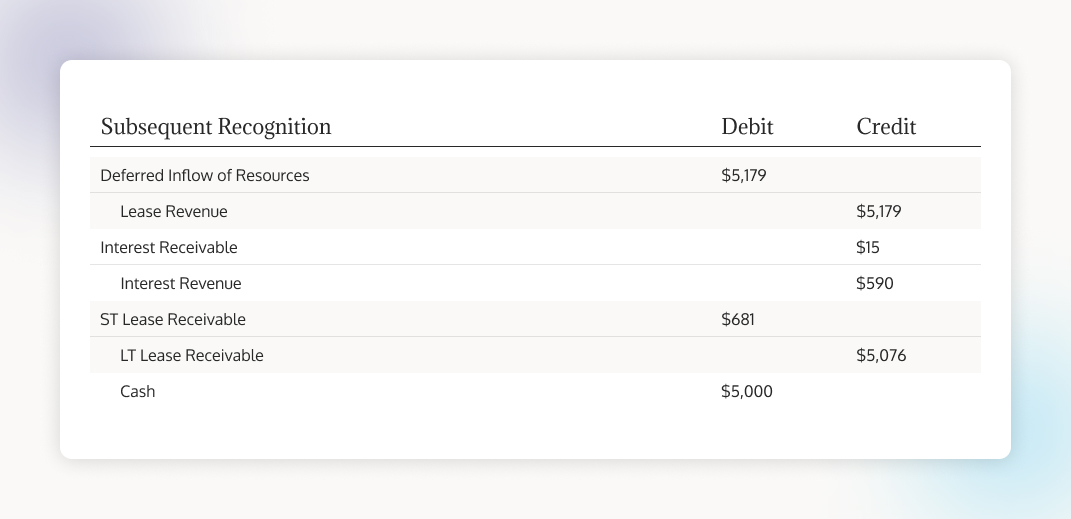

In month two, we still have the straight line revenue. There will be a debit for the deferred inflow of resources and a credit for the lease revenue. The interest on the remaining receivable and any adjustments, as well as an adjustment to the short and long term liability will also be recorded.

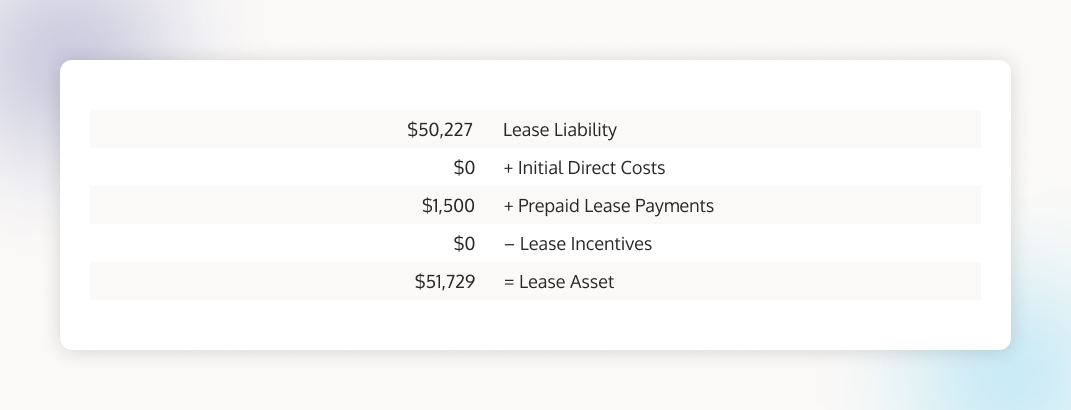

This example is for a 3-year lease for a vehicle with $1,500 a month payments on the first of each month and a 3% annual increase. In this case, the discount rate is implicit in the lease (5%).

To calculate the Lease Liability, determine the present value of future payments and then combine that present value for each payment.

Also important to add is the prepaid payment or the payment made at the beginning of the lease into the Lease Liability. Since it’s at its present value at the commencement, it’s not included in the Lease Liability but is added into the lease asset.

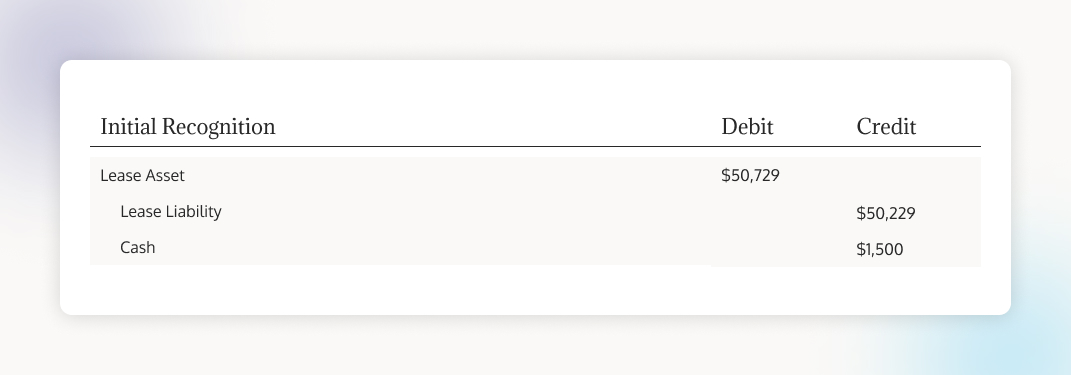

Below is the initial recording.

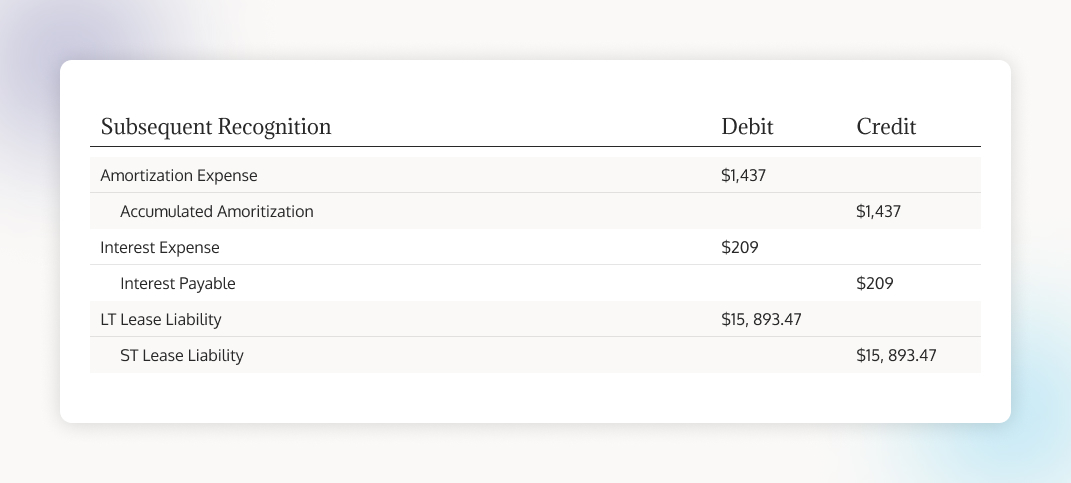

Below is the subsequent recognition with the amortization expense and accumulated amortization in the amount of $1,437. Also included are the interest expense and interest payable which is going to be the interest on the remaining liability ($209). Finally, there are the adjustments to the long and short term lease liability.

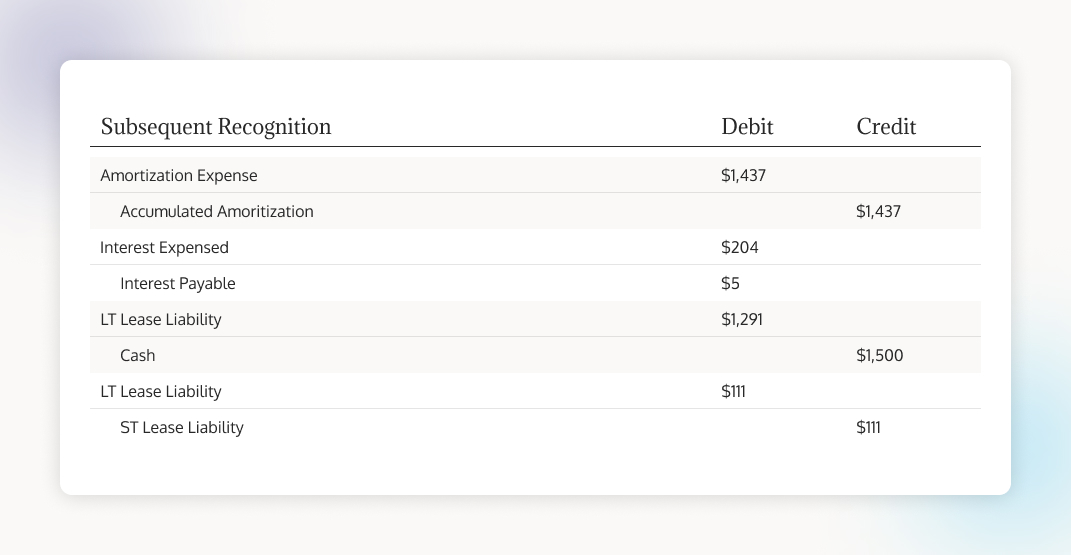

The second subsequent month—February in this case—is going to look similar to month one. First is the amortization expense and accumulated amortization, which is the straight line expense for the lease. Next is the interest expense and the change to interest payable. And then there is a reduction to the long term lease liability due to the monthly payments of $1500. Finally, the adjustment to make sure that the liability due in the next 12 months is $111.

One of the first and most important parts of properly implementing the new lease standard is reading GASB 87 itself.

All new lease accounting standards released by the GASB can be found on their website. The GASB 87 statement can be found here. Additionally, don’t forget to review the annual implementation guides for updates to the standard.

In order to ensure that all of your leases are documented according to the new lease standard, it is important to make a list of all of them so you don’t miss any. Pay particular attention to “embedded” leases, or leases that are components of contracts that entail the use of a certain asset. Often, these types of leases can be difficult to identify, which is why making a list of leases can be beneficial in ensuring complete compliance.

The next step in our GASB 87 implementation guide is to find and implement a lease accounting software. These programs boost accounting productivity and speed and reduce risk and error. Some can even automatically create perfect spreadsheets (more on that later).

Make sure you have a lease accounting software picked out and ramped up before the GASB 87 deadline to account for a slight adjustment period in process change.

The last step of our GASB 87 implementation guide involves simply putting the previously compiled list of leases and entering it into your lease accounting software.

Doing this will do three things: Ensure that you have no errors in your list of leases, make calculating journal entries later a breeze, and make the transition to the new lease standard very easy.

Don’t know where to start with finding a lease accounting software to help you maintain compliance with GASB 87? You’re in the right place.

To avoid the errors that might arise from having to manually account for the complicated and constantly changing GASB statements, think about utilizing lease accounting software, like LeaseCrunch, to make accounting faster and less risky.

LeaseCrunch software makes balance sheet calculations easy and utilizes automation to provide accurate and compliant deliverables. Just some of the differentiating benefits of using LeaseCrunch include:

Aren’t convinced yet that lease accounting software is for you? Sign up for a free demo and see our software in action instead. We look forward to helping you stay compliant with GASB guidelines in addition to providing this GASB 87 implementation guide.

How can I ensure that I have identified all leases that need to be accounted for under GASB 87?

Utilizing lease accounting software can help you ensure that no embedded leases or other sneaky leases are unaccounted for.

Can you provide examples of embedded leases, and how should they be treated under GASB 87?

An example of an embedded lease can be found in our blog on embedded leases, linked here.

Where can I find more information or assistance if I have questions or encounter difficulties during the GASB 87 implementation process?

Feel free to contact us here at LeaseCrunch if you have any problems or questions during your GASB 87 implementation process.

What types of leases are covered under GASB 87, and how does it change the accounting treatment for these leases?

All leases 12 months or longer now must be recognized as a lease liability and lease asset under GASB 87.